Introduction

Digital transformation — the integration of digital technology across every business function to improve operations, customer experience, and competitiveness — has shifted from a strategic option to a financial priority. The global market is now valued at over $1.3 trillion and is on track to nearly quadruple by 2033, according to Grand View Research.

For executives, this isn't abstract. Knowing which segments are growing fastest, where regional investment is accelerating, and which technologies are commanding the largest budgets directly shapes how you allocate resources. The organizations that track these signals early tend to move faster and spend smarter.

This article breaks down the current market size, the five trends reshaping enterprise technology investment, what's fueling growth, and the signals that should inform your strategy for the next 1–3 years.

Key Takeaways

- The global digital transformation market sits at $1.3T in 2025, with a projected CAGR of 19.4% through 2033

- AI, cloud infrastructure, and SaaS are the top three investment categories by spending volume

- North America holds 42.7% of global market share; Asia-Pacific is the fastest-growing region

- Big data and analytics accounts for over 23.4% of total digital transformation revenue

- Early movers consistently outperform laggards by 2x to 6x on total shareholder returns, per McKinsey research

Digital Transformation Market at a Glance: Size, Share, and Growth

Market Valuation and Trajectory

The global digital transformation market reached $1,302.95 billion in 2025, per Grand View Research. At a 19.4% CAGR from 2026 to 2033, it's projected to hit $5,493.15 billion by 2033. For context, IDC separately forecasts worldwide digital transformation spending to reach nearly $4 trillion by 2027, reflecting a 16.2% CAGR over 2022–2027.

The two forecasts use different scope definitions, but both point the same direction: enterprise digital investment is compounding fast, and organizations delaying commitment are falling further behind on every cycle.

Key market share benchmarks (2025):

- Large enterprises: 56.8% of total market spend

- Hosted/cloud deployment: 53.0% of deployments

- Big data and analytics: 23.4%+ of total market revenue

- SMBs: Growing at the fastest CAGR as platforms become more accessible

Regional Breakdown

| Region | Market Position |

|---|---|

| North America | 42.7% revenue share — dominant market leader |

| Asia-Pacific | Fastest-growing CAGR (2026–2033) |

| Europe | Strong share driven by compliance-led investment |

North America's lead reflects deep enterprise software penetration and high SaaS adoption. Asia-Pacific's acceleration is being driven by rapid industrialization, manufacturing digitization, and government-backed infrastructure programs.

Key Trends Shaping the Digital Transformation Market

Trend 1: AI and Intelligent Automation Move from Pilot to Production

AI deployment has moved decisively past the pilot phase. IBM's 2024 AI in Action report found that 42% of enterprise-scale companies (1,000+ employees) had actively deployed AI, while McKinsey reported 65% of organizations were regularly using generative AI in early 2024.

The financial case is compelling. Klarna's AI assistant handled 2.3 million customer service conversations in its first month — equivalent to the work of 700 full-time agents — cutting resolution time from 11 minutes to under 2 minutes and reducing repeat inquiries by 25%. In manufacturing, Siemens and Microsoft's Industrial Copilot enabled engineers to generate panel visualizations in 30 seconds, with generated code requiring only 20% adaptation.

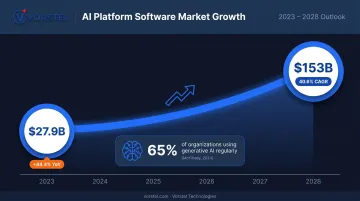

AI platform software revenue tells the same story: $27.9 billion in 2023 (up 44.4% year-over-year), with IDC forecasting $153 billion by 2028 — a 40.6% CAGR. Generative AI and emerging agentic AI capabilities are expanding use cases well beyond back-office automation — into customer-facing workflows, supply chain decisions, quality control, and financial forecasting.

Vorstel Technologies' own AI implementations reflect this production reality — including an AI-powered invoice automation system for a manufacturing client that replaced a fully manual ERP data entry process, and a machine learning quality control model that flags production defects in real time directly on the production line.

Trend 2: Cloud-First Strategies and SaaS Expansion

The SaaS case is straightforward: reduced deployment time, no version management overhead, and faster feature cycles. ERP, CRM, and collaboration tools lead adoption across enterprise categories.

IaaS growth is driven by a different force — AI workloads. Training and inference at scale demands elastic compute that on-premise infrastructure cannot cost-effectively provide.

Trend 3: ERP Modernization and Platform Consolidation

Legacy ERP systems are one of the most consistent drags on transformation progress. Organizations are actively replacing them with cloud-based platforms — SAP S/4HANA, Salesforce, and others — to unify data, enable real-time reporting, and reduce the IT maintenance overhead that consumes disproportionate budget.

The execution risk is real, though. Gartner predicts that by 2027, more than 70% of recently implemented ERP initiatives will fail to fully meet their original business goals — attributing this to technology-centric approaches that ignore stakeholder engagement and change management.

This is where implementation experience matters. Vorstel Technologies has delivered 200+ SAP projects and maintains a **95% success rate in Salesforce CRM implementations** — metrics that reflect not just technical delivery but the organizational alignment and user enablement work that determines whether an ERP actually performs in production.

Platform consolidation is a secondary driver. Retail, manufacturing, and e-commerce organizations are actively replacing fragmented point solutions with integrated ecosystems. The benefits are operational:

- Fewer vendor relationships to manage

- Cleaner data flows across business functions

- Lower integration maintenance costs over time

Trend 4: Cybersecurity as a Core Transformation Investment

As digital infrastructure scales, attack surface expands. The average global data breach cost reached $4.88 million in 2024, up from $4.45 million in 2023, according to IBM. Gartner projects worldwide information security spending will reach $212 billion in 2025 — a 15.1% increase from 2024. By 2027, 17% of total cyberattacks and data leaks are predicted to involve generative AI.

The organizational response is shifting from perimeter defense to architecture:

- 63% of organizations worldwide have fully or partially implemented zero-trust strategies (Gartner, 2024)

- Identity management, threat detection, and data governance have become core transformation line items rather than post-project additions

- Compliance requirements (GDPR, sector-specific regulations) are compelling infrastructure upgrades that simultaneously improve security posture

Trend 5: Data Analytics and Real-Time Business Intelligence

Big data and analytics represents more than 23.4% of total digital transformation market revenue — the largest single technology segment by share. The underlying shift driving investment is the move from periodic reporting to continuous, real-time operational intelligence.

Organizations investing in real-time data pipelines are seeing meaningful gains in supply chain responsiveness, customer service speed, and financial forecasting accuracy. The Forrester TEI benchmark for real-time data streaming infrastructure (Confluent Cloud vs. open-source Apache Kafka) found 257% ROI and over $2.5 million in savings — an indication of what's achievable when data latency is eliminated.

What separates high-performing analytics programs from underperforming ones is rarely data volume. Companies extracting the strongest ROI from analytics platforms share one trait: they prioritized clean, integrated data before scaling their tooling.

What's Driving Digital Transformation Market Growth

Four converging forces are pushing organizations to act — and narrowing the window for those still on the fence:

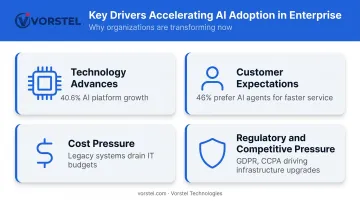

1. Technology advances lowering the barrier to entry AI, machine learning, IoT, and 5G are making enterprise-grade capabilities accessible to a much wider range of organizations. AI platform software is growing at a 40.6% CAGR — a rate that signals broad adoption, not niche experimentation.

2. Customer expectations demanding digital-first experiences Customers now expect 24/7 availability, omnichannel consistency, and personalization as defaults. Among business buyers, 46% said they would work with an AI agent for faster service (Salesforce, 2024). Organizations that don't meet this bar risk losing not just satisfaction scores, but contracts.

3. Cost pressure forcing modernization decisions Legacy systems consume a disproportionate share of IT budgets while delivering diminishing returns. Cloud infrastructure and automation reduce maintenance overhead and redirect capital toward innovation. This isn't an optional efficiency gain — for many enterprises, it's a budget survival calculation.

4. Regulatory and competitive pressure accelerating urgency GDPR, CCPA equivalents, and sector-specific compliance requirements are forcing investment in secure, auditable digital infrastructure. Simultaneously, digital-native competitors entering traditional industries are compressing the window available to incumbents for transformation.

Together, these drivers explain why digital transformation spending continues to accelerate across industries — and why market sizing projections keep getting revised upward.

How These Trends Are Impacting Businesses

Operational Impact

Automation is replacing manual, repetitive tasks across finance, HR, and supply chain. Real-time data pipelines are replacing end-of-month reporting cycles. Cloud-native architectures are reducing system downtime and enabling faster software deployment. Vorstel's enterprise clients report a 45% reduction in system downtime after moving to cloud-managed infrastructure — consistent with the broader industry pattern of operational stabilization post-migration.

Business Impact

At the board level, capital is shifting from legacy maintenance toward digital innovation — and new revenue streams (digital services, subscription models, data monetization) are emerging from those investments.

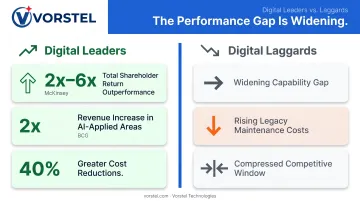

The performance gap between leaders and laggards is widening fast:

- McKinsey reports digital and AI leaders outperform laggards by 2x to 6x on total shareholder returns

- BCG finds AI leaders expect 2x the revenue increase and 40% greater cost reductions than laggards in AI-applied areas

Workforce Impact

Demand for cloud architects, AI engineers, data analysts, and ERP specialists is outpacing supply. Organizations are responding through internal reskilling programs and external consulting partnerships that bridge expertise gaps during active transformation programs.

For ERP modernization and AI deployment specifically, implementation quality directly determines whether the investment delivers on its business case — making the right partner choice a strategic decision, not just a procurement one.

Future Signals for the Digital Transformation Market

Three developments are moving from early signal to near-term reality. Organizations that track them now will build durable strategic advantages:

Agentic AI moving from content to action Gartner predicts 15% of day-to-day work decisions will be made autonomously through agentic AI by 2028, up from near zero today. The caveat: Gartner also predicts over 40% of agentic AI projects will be canceled by end-2027 due to execution failures. High potential, but only for organizations that build the data foundations and governance frameworks first.

Digital sovereignty reshaping cloud selection By 2027, 70% of enterprises adopting generative AI will cite digital sovereignty as a top criterion for cloud provider selection (Gartner). Sovereign cloud architectures and regional deployment models are becoming procurement requirements, not preferences.

Smart manufacturing at scale Deloitte surveyed 600 executives and found 92% believe smart manufacturing will be the primary driver of competitiveness over the next three years. Physical AI — robotics, vision systems, and factory automation — is scaling faster than most digital strategy roadmaps currently account for.

Acting on these signals requires more than strategic awareness — the gap between recognizing a trend and deploying it successfully is where most organizations stall. Firms like Vorstel Technologies address this directly, joining client engagements at any stage — from architecture design through implementation and DevOps — to ensure the foundational work is in place before emerging AI, cloud, and ERP capabilities go live.

Conclusion

The digital transformation market — $1.3 trillion today, projected to reach nearly $5.5 trillion by 2033 — reflects a structural shift in how organizations operate and compete, not a technology cycle. The trends documented here — AI moving to production, cloud becoming the default infrastructure, ERP modernization accelerating, cybersecurity becoming foundational, and data analytics driving real-time decisions — are compounding simultaneously.

Organizations that align strategy with these trends early will compound their competitive advantage. Those that delay face not just rising costs but a widening capability gap against competitors already building depth in AI, cloud, and data.

Closing that gap requires two things: a clear strategic roadmap and an implementation partner that can move quickly across AI, cloud, and ERP without starting from scratch. Firms like Vorstel Technologies, which specialize in entering client engagements at any stage of the transformation journey, reflect exactly the kind of execution-focused partnership this market demands. Organizations that build this capability now — iteratively, not in a single go-live — will be structurally better positioned as the market continues to accelerate through the decade.

Frequently Asked Questions

What is the digital transformation market?

The digital transformation market covers global spending on technologies, services, and platforms — including AI, cloud infrastructure, ERP, and analytics — that help organizations modernize operations, improve customer experience, and outpace competitors. This includes both technology investment and the professional services needed to implement and sustain those systems.

How large is the digital transformation market, and what is its projected growth rate?

According to Grand View Research, the market reached $1,302.95 billion in 2025 and is projected to grow at a 19.4% CAGR through 2033, reaching $5.49 trillion. IDC's separate forecast projects nearly $4 trillion in digital transformation spending by 2027. Both figures signal that enterprise digital investment is a primary budget priority across most industries.

What industries are investing the most in digital transformation?

Financial services, manufacturing, retail, healthcare, and e-commerce lead spending. Financial services are driven by customer experience and regulatory compliance demands; manufacturing by operational efficiency and smart factory initiatives; retail and e-commerce by omnichannel infrastructure and supply chain modernization.

What are the biggest barriers to digital transformation success?

Three barriers consistently derail transformation programs:

- Legacy systems — fragmented infrastructure consumes IT budgets and creates integration complexity

- Talent gaps — a global shortage of skilled professionals in AI, cloud, and ERP disciplines

- Cybersecurity risk — escalating threats that raise cost and complexity across every initiative

How is AI changing the digital transformation landscape?

AI has moved from experimental pilots into full production — automating workflows, enabling real-time decisions, and powering autonomous business processes at scale. It's now the single largest driver of new transformation investment: AI platform software is projected to grow from $27.9 billion in 2023 to $153 billion by 2028.

How do organizations measure ROI on digital transformation investments?

ROI is assessed across three dimensions: strategic outcomes (revenue growth, time to market), operational metrics (productivity, uptime, deployment speed), and cost impact (reduced legacy maintenance and manual process spend). Organizations that define these metrics before implementation consistently report stronger satisfaction with results.